Hustle Intro: Navigating the Maze When You’re Unemployed

Before plunging into the wild world of health insurance options for the unemployed, let’s address the elephant in the room: How to Get Health Insurance Without a Job. It’s a tough situation to be in, but there are ways to navigate through it. Check out this resource for more information on your options.

Why Health Insurance is a Must – Even Without the 9 to 5 Grind

Any savvy hustler knows that health insurance is non-negotiable, even when you’re between jobs. Accidents happen, illnesses strike, and medical bills can pile up faster than you can say “side hustle”. Without proper coverage, you’re risking your financial stability and well-being. It’s crucial to find a solution that fits your needs and budget.

One of the biggest challenges of being unemployed is navigating the maze of health insurance options. This guide is here to break down the barriers and simplify the process for you. With the right knowledge and resources, you can find the coverage you need to protect yourself and your loved ones during this challenging time.

Breaking Down the Barriers: How This Guide Can Help

Another aspect to consider is the time-sensitive nature of health insurance. Ignoring this crucial need can have devastating consequences in the long run. By taking proactive steps and utilizing the information in this guide, you can secure the coverage you need without adding unnecessary stress to your plate. Stay tuned for practical tips and insights to navigate the insurance maze with confidence.

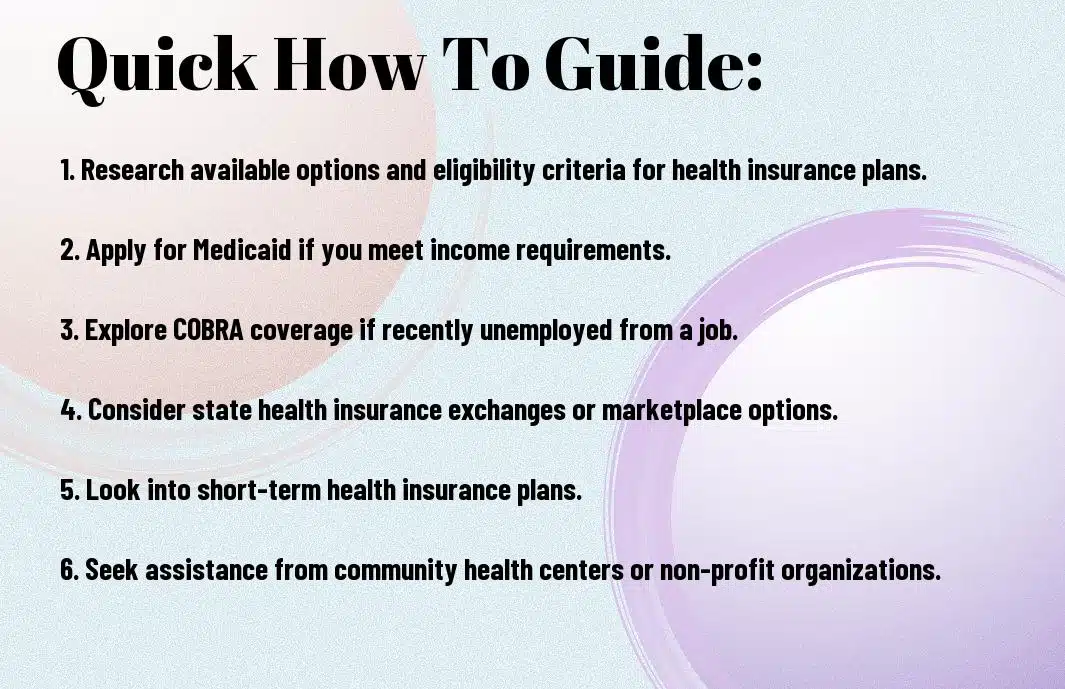

Key Takeaways:

- Check for government programs: Look into Medicaid or the Affordable Care Act for potential coverage options.

- Consider COBRA: If you recently lost your job, you may be eligible for COBRA to continue your previous employer’s health insurance plan for a limited time.

- Explore private health insurance: Research and compare different private health insurance plans that may fit your needs and budget.

- Look into short-term health insurance: Short-term plans can provide temporary coverage until you find a job with health benefits.

- Join a spouse or family member’s plan: If your spouse or family member has health insurance through their employer, you may be able to join their plan.

- Check for coverage through professional organizations: Some professional associations offer health insurance options for their members.

- Consider health sharing ministries: These organizations provide a community-based approach to sharing medical costs among members.

Getting into the Mindset: Preparing to Secure Health Coverage

Letting Go of Job-Based Insurance Myths

On your journey to secure health coverage without a job, it’s crucial to let go of common myths surrounding job-based insurance. Some people believe that health insurance is only accessible through traditional employment, but that’s simply not true. With the rise of the gig economy and freelance opportunities, there are now more options than ever for individuals to find alternative health coverage.

Don’t fall into the trap of thinking that job-based insurance is the only reliable option. Empower yourself with knowledge about the various health insurance marketplaces, government programs, and private providers available. By shedding misconceptions about job-based insurance, you open yourself up to a world of possibilities for securing the coverage you need.

Adopting a Proactive Approach to Your Health and Wealth

There’s no time like the present to take charge of your health and financial well-being. By adopting a proactive approach, you can create a safety net for yourself that doesn’t rely on a traditional job. Start by assessing your current health needs and researching different insurance plans that align with your budget and lifestyle.

Adopting a proactive approach to your health and wealth also means investing in preventative care to avoid costly medical bills down the line. Consider incorporating healthy habits into your daily routine and staying up-to-date on screenings and check-ups. Keep in mind, your health is your most valuable asset, so prioritize it accordingly.

The Health Insurance Playbook: Know Your Options

Now, more than ever, it’s crucial to have a game plan when it comes to securing health insurance without a job. Understanding your options and knowing how to navigate the system can make all the difference in getting the coverage you need. Whether you’re considering COBRA or Medicaid, being informed is key to making the right choice for your health and financial well-being.

Squeezing the Most Out of COBRA: Is It Right for You?

You need to understand the ins and outs of COBRA before deciding if it’s the right move for you. COBRA allows you to keep your employer-sponsored health insurance for a limited time after losing your job, but the costs can be high. You’ll have to pay the full premium, including what your employer used to cover, plus a 2% administrative fee. It’s a short-term solution that can bridge the gap while you look for other options, but you need to weigh the cost against the benefits.

Choosing COBRA means you won’t have to switch doctors or networks, which can be a relief if you have ongoing medical needs. However, it’s crucial to explore other alternatives as well, as COBRA may not always be the most cost-effective choice in the long run. Compare plans, prices, and coverage to make an informed decision that fits your current situation and future goals.

Medicaid: Not Just for the Few – Understanding Eligibility

Playbook: Medicaid is often misunderstood as a resource only for the extremely low-income or disabled individuals. In reality, Medicaid is a federal and state program that provides healthcare coverage to low-income individuals and families, including children, pregnant women, elderly, and people with disabilities. Eligibility is based on income, family size, and other factors, and it varies from state to state.

Eligibility: To qualify for Medicaid, you generally need to meet specific income requirements set by your state. The program offers a comprehensive range of benefits, including doctor visits, hospital stays, preventive care, and more. If you find yourself without a job and struggling to afford health insurance, exploring Medicaid eligibility could be a game-changer in getting the coverage you need.

Navigating the Marketplace Like a Pro

How to Tackle the Health Insurance Marketplace

Many people find the health insurance marketplace to be overwhelming and confusing, but fear not! With the right approach, you can navigate it like a pro. Assuming you’re looking for health insurance without a job, start by researching different plans available in your state. Compare the coverage, network of providers, and costs associated with each plan to determine which one best fits your needs.

Once you have a good understanding of the options, consider seeking assistance from a licensed insurance agent or broker. These professionals can help guide you through the process and answer any questions you may have. By utilizing their expertise, you can make a more informed decision when selecting a health insurance plan that aligns with your current situation.

Tips for Choosing the Best Plan on a Tight Budget

Some individuals may be on a tight budget when looking for health insurance without a job. It’s important to make the most of your money by choosing a plan that offers the best coverage at an affordable price. Start by comparing the premiums, deductibles, and out-of-pocket costs of each plan to determine which one provides the most value.

- Consider opting for a high-deductible plan paired with a Health Savings Account (HSA) to save on premiums while still having coverage for unexpected medical expenses.

- Look for plans that offer telemedicine services, which can provide convenient and cost-effective access to healthcare professionals for non-emergency medical issues.

- Knowing your healthcare needs and anticipated costs can help you choose a plan that offers the right balance of coverage and affordability.

Alternative Tactics: When Traditional Routes Don’t Cut It

Despite your best efforts, sometimes the traditional routes to health insurance just don’t seem to work out. But fear not, there are alternative tactics you can explore to secure health coverage even without a job. Let’s examine some creative strategies that might just be the solution you’re looking for.

Freelancers Unite: Joining Forces in Health Sharing Ministries

One option for those without traditional job-based health insurance is to join a health sharing ministry. These are typically faith-based organizations where members contribute a monthly amount, which is then used to cover each other’s medical expenses. While not technically insurance, it can provide a sense of security and help alleviate the burden of high healthcare costs.

Getting by with Short-Term Health Insurance: The Pros and Cons

Unite

When traditional health insurance is out of reach, short-term health insurance can be a temporary solution. This type of coverage typically lasts for a few months to a year and is designed to provide basic protection in case of unexpected medical expenses. However, it’s important to weigh the pros and cons before opting for this type of coverage.

| Pros | Cons |

| Low monthly premiums | Limited coverage |

| Quick and easy to enroll | May not cover pre-existing conditions |

| Provides basic protection | Not renewable in some states |

Health sharing ministries and short-term health insurance can be viable options for those in need of coverage without a traditional job. While they may not offer the same comprehensive benefits as employer-sponsored plans, they can provide a safety net in times of uncertainty. It’s crucial to carefully consider your needs and budget before choosing the right option for you.

Crushing the Numbers: Affording Health Insurance without a Steady Income

Strategies to Make Health Insurance Affordable Without a 9 to 5

Not having a traditional 9 to 5 job doesn’t mean you have to forgo health insurance. There are strategies you can implement to make health insurance more affordable even without a steady income. One option is to explore government-subsidized health insurance programs like Medicaid or the Affordable Care Act, which can provide coverage at a lower cost based on your income level.

Another way to make health insurance more manageable is to consider high-deductible health plans paired with a Health Savings Account (HSA). These plans typically have lower monthly premiums, which can be a lifesaver when you’re on a tight budget. By contributing to an HSA, you can set aside pre-tax dollars to cover medical expenses, making healthcare more affordable in the long run.

Factors That Impact Your Health Insurance Costs and How to Leverage Them

On the flip side, factors like your age, location, and smoking status can also impact how much you pay for health insurance. By understanding these factors and how they influence your premiums, you can take steps to leverage them in your favor. For example, quitting smoking can not only improve your health but also reduce your insurance costs significantly.

Insurance companies also consider your overall health and pre-existing conditions when determining your premiums. Maintaining a healthy lifestyle and managing any chronic conditions can help lower your insurance costs. Knowing how these factors affect your premiums can empower you to make informed decisions about your health and your finances.

- Age – Younger individuals typically pay lower premiums.

- Location – Insurance costs can vary based on where you live.

- Smoking Status – Tobacco users often pay higher premiums.

- Pre-existing Conditions – Health conditions can impact insurance costs.

- Health Lifestyle – Maintaining good health can lower insurance expenses.

- Knowing how to navigate these factors can help you save money on health insurance in the long run.

The Side Hustle: Leveraging Part-Time Gigs for Insurance

Playing the Field: Finding Part-Time Work with Health Perks

Your side hustle isn’t just about making some extra cash on the side. It can also be a gateway to securing health insurance benefits that are typically reserved for full-time employees. When scoping out part-time gigs, look for opportunities with companies that offer health perks for their employees, even those working part-time hours. Retailers, restaurants, and even tech companies are known to provide health benefits to their part-time staff.

Don’t be afraid to ask about health insurance benefits during the interview process. Be upfront with potential employers about your priorities and the importance of having access to health coverage. By strategically choosing where you work part-time, you can maximize your earning potential while also taking care of your health.

Gig Economy 101: Navigating Health Insurance for Freelancers and Contractors

When exploring into the gig economy as a freelancer or contractor, it’s crucial to understand how to navigate the world of health insurance. Unlike traditional full-time positions, gig workers are responsible for finding and funding their own health coverage. Fortunately, there are options available to help you secure the healthcare benefits you need.

Consider looking into freelancer unions or associations that offer group health insurance plans for independent workers. Additionally, you can explore the Health Insurance Marketplace to compare different plans and find one that fits your needs and budget. Don’t let the lack of a traditional job hold you back from accessing quality health insurance as a gig worker.

PartTime – While navigating the gig economy may seem daunting at first, the freedom and flexibility it offers can be well worth the effort. By taking the time to research and understand your options for health insurance, you can ensure that you have the coverage you need to stay healthy and focused on growing your side hustle.

Staying Ahead of the Game: Maintaining Your Coverage

Annual Check-up: Evaluating Your Health Insurance Needs Regularly

To stay ahead of the game when it comes to your health insurance, you need to take charge. Even if you have coverage in place, it’s vital to regularly evaluate your needs. Factors such as changes in your health, lifestyle, or financial situation can affect the adequacy of your current plan. Schedule an annual check-up to review your coverage and make any necessary adjustments to ensure you are adequately protected.

Don’t wait until a health crisis hits to reevaluate your coverage. By staying proactive and frequently reassessing your health insurance needs, you can avoid being caught off guard. Your health is your most valuable asset, so make sure you are proactive in managing your insurance coverage to secure your peace of mind.

When Life Throws a Curveball: How to Handle Changes and Keep Your Coverage

Life is unpredictable, and unexpected changes can impact your health insurance coverage. Coverage gaps can occur due to job loss, moving to a new state, getting married, or having a child. When these curveballs come your way, it’s crucial to have a plan in place to ensure you maintain uninterrupted coverage. Stay on top of any life changes and be prepared to navigate the complex world of health insurance.

Plus, having a solid understanding of your options when life throws you a curveball can empower you to make informed decisions about your health insurance. Research different coverage alternatives, such as COBRA, Medicaid, or marketplace plans, to determine the best course of action for your individual needs. By being proactive and knowledgeable, you can navigate through life’s twists and turns while maintaining the coverage you need.

Also Read: How To Respectfully Decline A Job Offer

Summing up

So there you have it, folks. Getting health insurance without a job may seem daunting, but with the right mindset and determination, it’s totally doable. Bear in mind, it’s all about hustling, being resourceful, and thinking outside the box to secure the coverage you need. Whether it’s through a spouse’s plan, Medicaid, COBRA, or the marketplace, there are options out there for you. Don’t settle for mediocre coverage – go out there and make it happen!

FAQ

Q: How can I get health insurance without a job?

A: The best way to get health insurance without a job is to explore options such as purchasing a plan through the Affordable Care Act (ACA) marketplace, applying for Medicaid if you qualify based on income and family size, or checking if you are eligible for COBRA coverage through your previous employer.

Q: What is the Affordable Care Act (ACA) marketplace?

A: The ACA marketplace, also known as the health insurance exchange, is a platform where individuals and families can compare and purchase health insurance plans. You can visit healthcare.gov to explore different plans available in your area and see if you qualify for financial assistance.

Q: How do I apply for Medicaid?

A: To apply for Medicaid, you can visit your state’s Medicaid website or use the Medicaid.gov website to determine if you qualify based on your income, family size, and other factors. Medicaid provides free or low-cost health coverage to eligible individuals and families.

Q: What is COBRA coverage?

A: COBRA stands for the Consolidated Omnibus Budget Reconciliation Act, which allows you to continue your employer-sponsored health insurance plan for a limited period after you lose your job. You may be eligible for COBRA coverage if you were covered by a group health plan through your previous employer.

Q: Are there any other options for getting health insurance without a job?

A: In addition to the ACA marketplace, Medicaid, and COBRA, you can also consider short-term health insurance plans, health care sharing ministries, or asking about coverage options through your spouse or partner’s employer-sponsored plan. It’s imperative to explore all available options to find the best coverage that meets your needs.